Collars And Price Floors Caps

Calpine Energy Solutions Products Price Collars

Http Janroman Dhis Org Stud Ii2008 Caps And Floors Pdf

Ppt Caps Floors And Collars Powerpoint Presentation Free Download Id 6803699

Interest Rate Products Caps Collars Youtube

:max_bytes(150000):strip_icc()/strategy-4086857_19201-23485cf7c4bf4dbbb95c93f267285f16.jpg)

Interest Rate Collar Definition

Multi Period Options Interest Rate Caps Interest Rate Floors Ppt Video Online Download

An interest rate cap is a derivative in which the buyer receives payments at the end of each period in which the interest rate exceeds the agreed strike price an example of a cap would be an agreement to receive a payment for each month the libor rate exceeds 2 5.

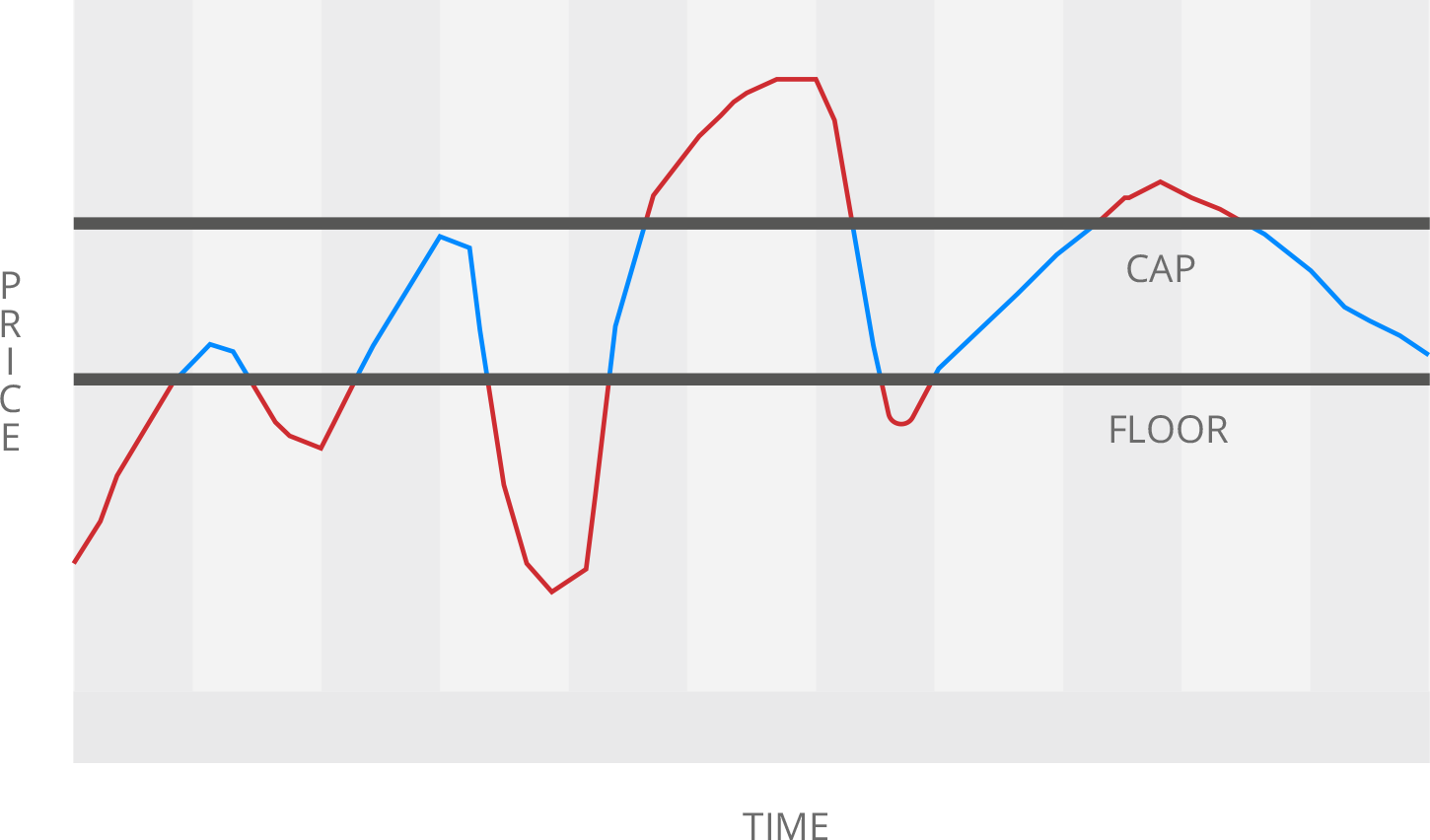

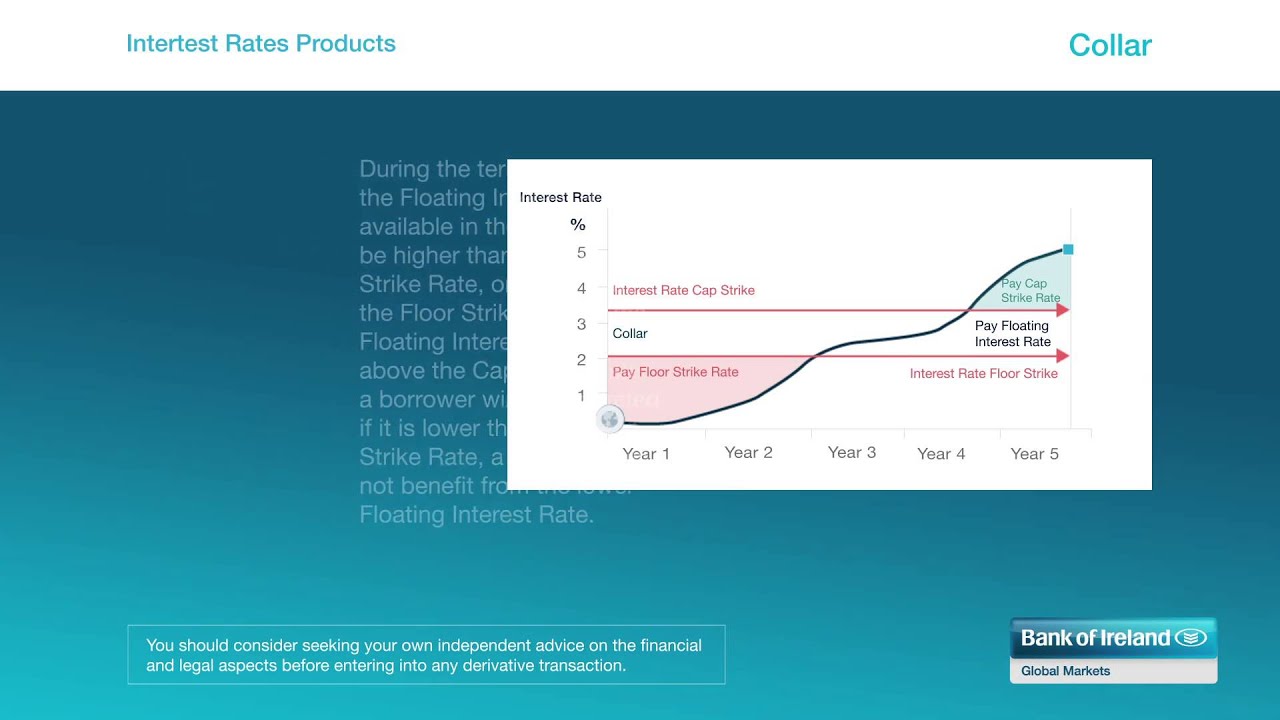

Collars and price floors caps. Floor payments time 0 time 0 5 time 1 5 54 6 004 0 4 721 6 915 5 437 0 1395 4 275 consider a 100 notional of 1 5 year semi annual floor with. Interest rate caps floors and collars these option products can be used to establish maximum cap or minimum floor rates or a combination of the two which is referred to as a collar structure. Unlike for other options the system does not use the option data tab page to map caps floor and collars the option information is contained within the condition data and in the cash flow generated on the basis of the condition data. These products are used by investors and borrowers alike to hedge against adverse interest rate movements.

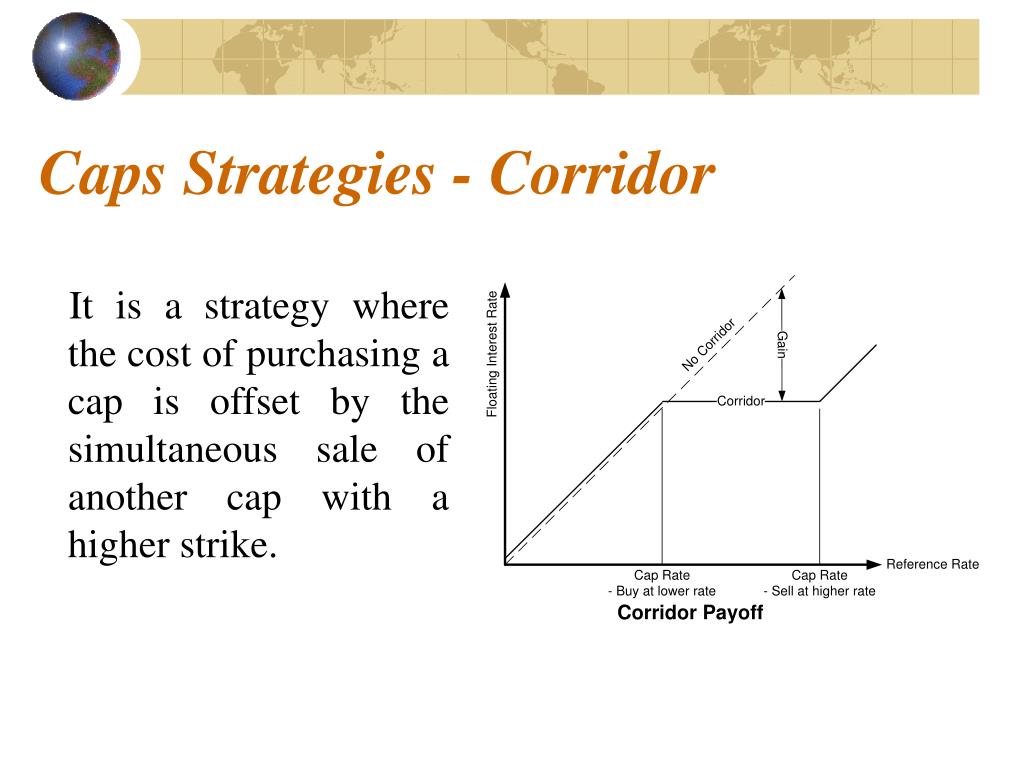

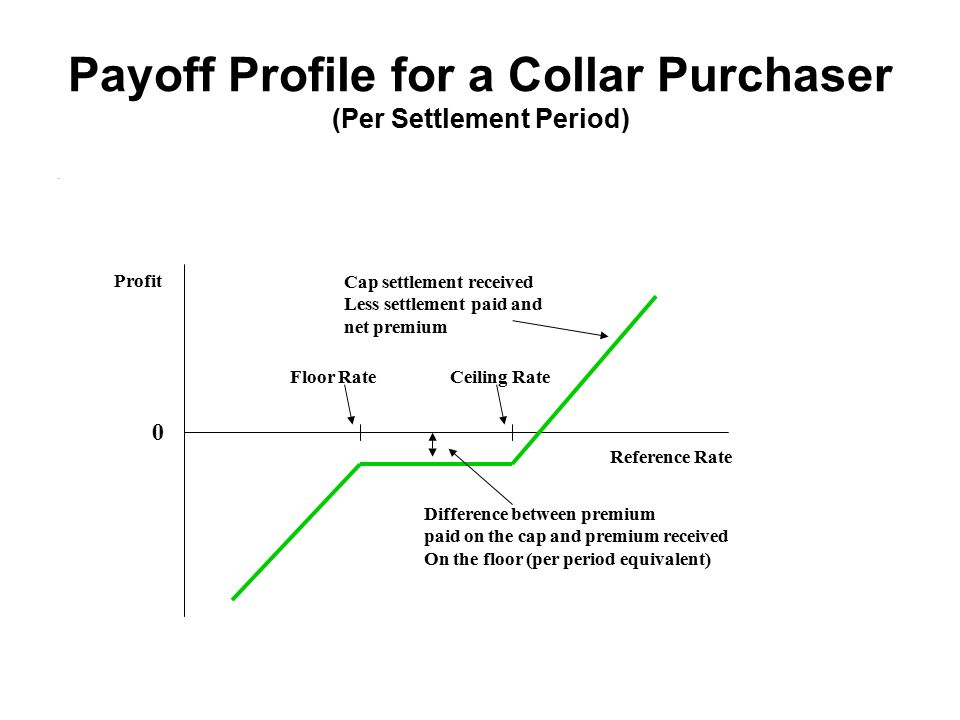

Buying a put option at strike price x called the floor selling a call option at strike price x a called the cap. An interest rate collar can be created by buying a cap and selling a floor. They are most frequently taken out for periods of between 2 and 5 years although this can vary considerably. These latter two are a short risk reversal position.

While the collar effectively hedges. This creates an interest rate range and the collar holder is protected from rates above the cap strike rate but has forgone the benefits of interest rates falling below the floor rate sold. Underlying risk reversal collar. You use template s40caflcol to map caps floors and collars as unstructured transactions in the source data layer sdl.

Cap and floor payoffs and interest rate collars.

Rate Cap Swap And Collar A Cheat Sheet To Managing Rate Risk Derivative Logic

Houston Astros Personalized Classic Leather Baseball Collar Leather Dog Collars Classic Leather Leather Collar

Make Your Own Dog Collar I Have Been Wanting A Bowtie Collar For Dexter But They Are So Expensive Dog Collars Leashes Diy Dog Collar Dog Leash

Caps Floors And Collars Ppt Download

Bright Orange Hunting Dog Collar Waterproof Dog By Doggonenice Hunting Dog Collars Waterproof Dog Collar Hunting Dogs

Inverted Cross Snapback Snap Casual Baseball Caps Hip Hop Cap Flat Hats

Custom Engraved Leather Dog Collar Side Release Buckle Purple Dog Pet Fashion Engraved Leather Dog Collar Leather Dog Collars Dog Collar

Lids Cap Care Kit Hat Cleaner Deodorizer Brush Water Stain Repellent Hat World How To Clean Hats Stain Deodorant

Overstock Com Online Shopping Bedding Furniture Electronics Jewelry Clothing More Energy Efficient Light Bulbs Floor Lamp Lamp

Pin On Ideas

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

Sodial R Digital Pet Collar Cam Camera Mini Video Recorder Cam Camera Dvr Video Recorder Monitor For Dog Cat Puppy Black Dog Training Techniques Dog Training Dog Training Tips

Semi Choke Martingale Collar Blind Dog Dog Pads Dog Leash