Concept Of Materiality As A Constraint In Accounting

Pin By Mckell Kimball On The Accountant In Me Conceptual Framework Accounting And Finance Business Tax

Resultado De Imagem Para Accounting Principles Accounting Principles Accounting Accounting And Finance

Accounting Constraints Double Entry Bookkeeping

Pin By Paul Banting On Accounting Conceptual Framework Accounting Investing

The Structure Of The Conceptual Framework Of Accounting Google Search Conceptual Framework Framework Conceptual

Intermediate Accounting Ch 2 Diagram Quizlet

If a transaction is material enough to exceed the constraint threshold then it is recorded in the financial records and therefore appears in the financial statements if a transaction does not meet this threshold level it may not be recorded in the.

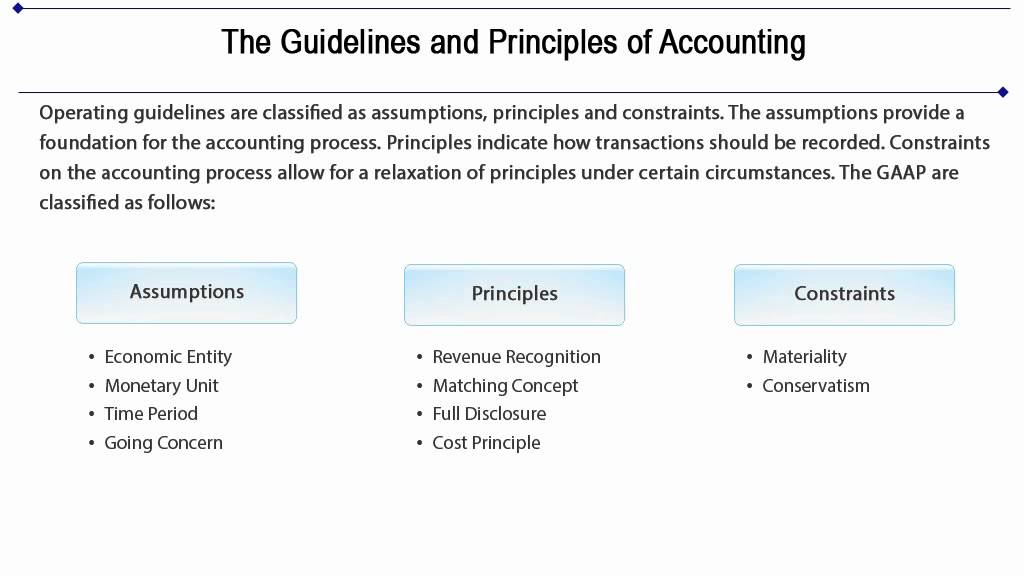

Concept of materiality as a constraint in accounting. The materiality concept is the universally accepted accounting principle reporting firms must disclose all such matters. While cost benefit and materiality are the two overriding accounting constraints industry practices are a less dominant constraint but also part of the reporting environment. Here is a list of the four basic accounting concepts and constraints that make up the gaap framework in the us. According to this principle the cost of applying an accounting principle should not be more than its benefits.

The items that have very little or no impact on a user s decision are termed as immaterial or insignificant items. They are described below. The materiality concept of accounting stats that all material items must be properly reported in financial statements an item is considered material if its inclusion or omission significantly impacts the decision of the users of financial statements. This video give the basic concept of materiality concept materiality constraint in accounting urdu hindi my recommenmd amazing gears products.

Particular industry practices in financial reporting may cause departure from basic accounting standards for companies in certain industries. Fundamental accounting concepts and constraints. Financial information might be of material importance to one company but stand immaterial to another company. This aspect of the materiality concept is more noticeable when.

Cost benefit principle materiality principle consistency principle conservatism principle timeliness principle and. If the cost. 6 constraints of accounting are. Home accounting principles materiality concept the materiality concept also called the materiality constraint states that financial information is material to the financial statements if it would change the opinion or view of a reasonable person.

The materiality concept in accounting is also known as materiality constraint.

Solved Following Are The Concepts Of Accounting Covered In Cha Chegg Com

6 Constraints Of Accounting

Solved Exercise 4 2 Identify The Accounting Concept That Chegg Com

Free Classifieds Ads Online Angels Ad Posting Website Accounting Online Online Ads

Accounting Principles Constraints Concepts And Assumptions By Billy Haps

Build A Simple To Do List App In Golang In 2020 Comprehension Activities Make A Donation To Do List

Top 19 Magento 2 Quote Extensions Free Medium Premium Options In 2020 Email Quotes Enabling Quotes Mass Quotes

الاطار النظري للمحاسبة Conceptual Framework Principles Equity

Accounting Principles Accounting Education Facebook

Accounting Principles Ppt Video Online Download

Quiz 1 Solution Acct 6306 Intermediate Accounting I Studocu

Framework For Management Accounting

Intermediate Accounting Ch 1