Cov Mat R Finance

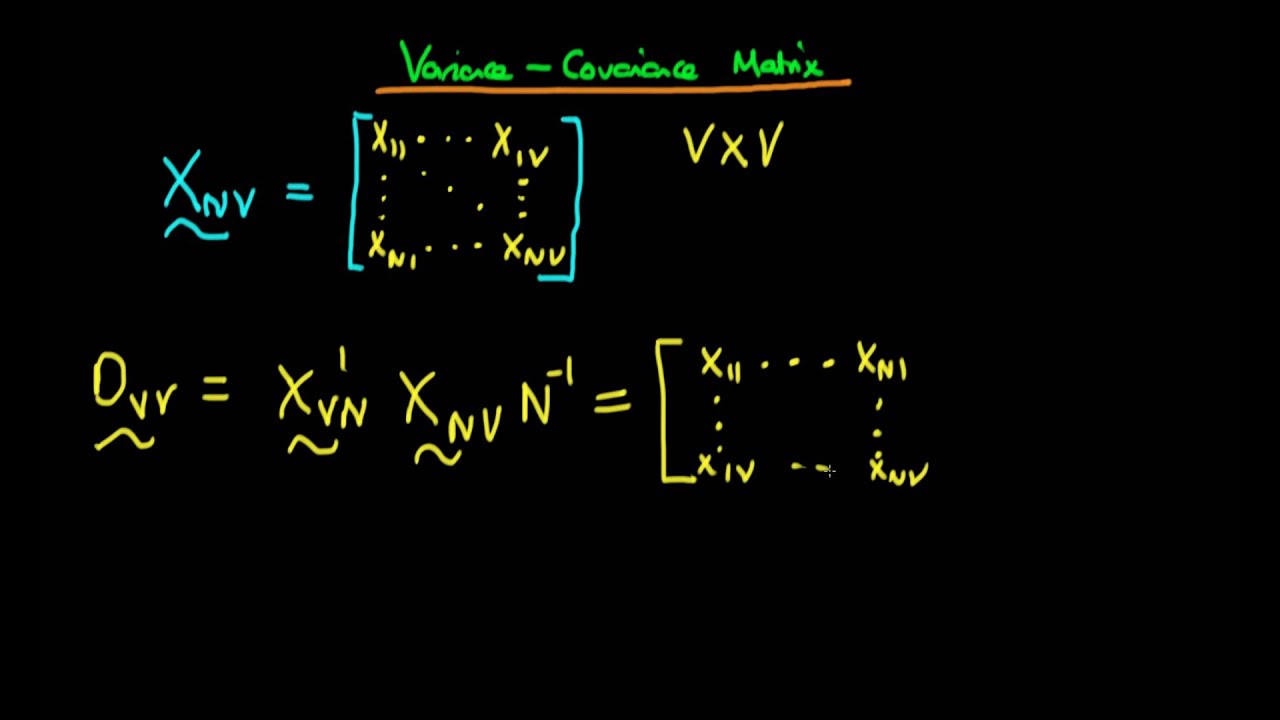

Variance Covariance Matrix Stock Price Analysis In R Corpcor Covmat In 2020 Stock Market Crash Stock Research Stock Market

Rip Robin Williams Genie We Re Gonna Miss You T Shirt By Suzeejobs R Aff Ad Williams Robin Rip Genie In 2020 Geek Quotes Classic T Shirts Geek Humor

Album Cover Artist Book Project Launches On Kickstarter Album Covers Book Projects Album

Variance Covariance Matrix Using Matrix Notation Of Factor Analysis Youtube

Toyota Yaris Hybrid R Concept Mikeshouts Yaris Toyota Toyota Hybrid

Maxpider 3d Rubber Molded Floor Mat For Volkswagen Jetta 05 10 Kagu Gray Row 1 2 Jetta Gli Volkswagen Jetta Volkswagen

Tax lien sale virtual outreach sessions.

Cov mat r finance. Suppose our data is in dat. Cross covariance matrix computes the cross covariance matrix between two sets of locations for a spatial random process with a given covariance structure. Smart beta is what people call algorithms that construct portfolios that are intended to beat market cap weighted benchmarks without a human. Portfolio r functions for portfolio analysis to be used in introduction to computational finance financial econometrics last.

Useful financial r snippets making smart beta portfolios in r making smart beta portfolios in r here we explore smart beta and how to build portfolios which implement smart beta in r. Dat dat c 2 4 remove team name and ds names left in data frame names dat 1 playername mb game reshape from long to wide dat wide reshape dat direction wide idvar game timevar playername dat wide 1. The returned object is of class portfolio. The diocese of coventry multi academy trust.

I think what you first need to do is reshape the data so that each row is a game and each column is the mb for a game for a player. Department of finance 311 search all nyc gov websites. If short sales are not allowed then the portfolio is computed numerically using the function samp solve qp from the samp quadprog package. Typically the two sets are a learning set and a test set.

Type package title covariance matrix estimation and regularization for finance version 1 1 0 description estimation and regularization for covariance matrix of asset returns. An exempt charity and a company limited by guarantee registered in england and wales no 8422015. Property records acris contact us. R functions for portfolio analysis my r functions on class webpage in portfolio r and portfolio noshorts r r packager package portfolioanalytics on r on r forge extensive collection of functions rtirme trics package fp tf lifportfolio extensive collection of functions r package quadprog solve qp for quadratic.

Er n x 1 vector of expected returns cov mat n x n covariance matrix of returns weights n x 1 vector of portfolio weights output is portfolio object with the following elements. Param er samp n x 1 vector of expected returns param cov mat samp n x n return covariance matrix param target return scalar target expected return param shorts logical if. Description compute global minimum variance portfolio given expected return vector and covariance matrix. For covariance matrix estimation three major types of factor models are included.

The portfolio can allow all assets to be shorted or not allow any assets to be shorted.

Vtec Mini Vtec Mini Mini Cooper

Invitations De Mariage Fete Rock N Roll Design Disque Wedding Party Invites Affordable Wedding Invitations Rock N Roll Wedding

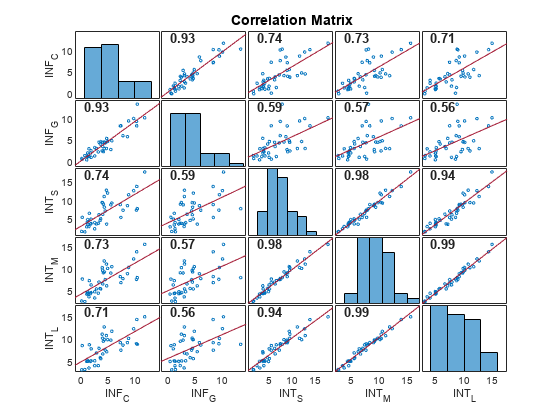

Plot Variable Correlations Matlab Corrplot

Fondos De Pantalla Simple Acrylic Paintings Aesthetic Pastel Wallpaper Aesthetic Art

How To Draw A 95 Confidence Ellipse To An Xy Scatter Plot

2019 Bmw S 1000 Rr An Icon Among Superbikes Bmw S1000rr Bmw Sport Bmw S

3 680 Mentions J Aime 19 Commentaires Alfa Romeo Thealfacollection Sur Instagram Awesome Drive Free In 2020 Alfa Romeo Gta Classic Cars Car

Mini Beachcomber 4x4 Concept Heads To Detroit Auto Show New Photos Added Carscoops Mini Cooper Mini Cars Mini

Minimalist Graphic Design Minimalist Graphic Design Graphic Design Design Shack

To Be Lucky Luck Quotes Good Luck Quotes Wonderful Words

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctdiuliqmdrtoedcavl4trt5fuhhlz3adyqza Usqp Cau

Pin On Marine Electronics Products

Estimation Of Covariance Matrices Wikipedia