Cv Mat Variance

Variance Learn Opencv

Detect Blurry Images With Laplacian Variance Issue 448 Justadudewhohacks Opencv4nodejs Github

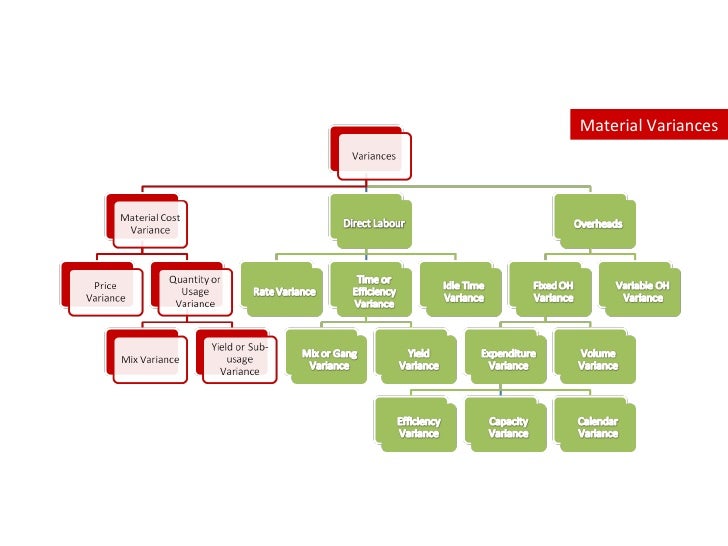

How To Calculate Variances Sv Schedule Variance Cv Cost Variance Spi Project Management Professional Earned Value Management Small Business Management

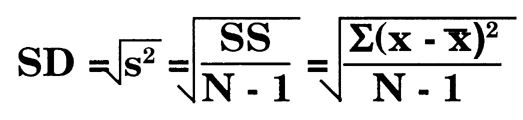

Standard Deviation Formula Standard Deviation Earned Value Management Formula

10 Ways To Present Variance Analysis Reports In Excel Free Excel Tutorials Tips Tricks Techniques Dashboard Tem Excel Tutorials Excel Formula Resume Tips

Area Under The Curve Auc And Variance Estimates Calculated With Two Download Scientific Diagram

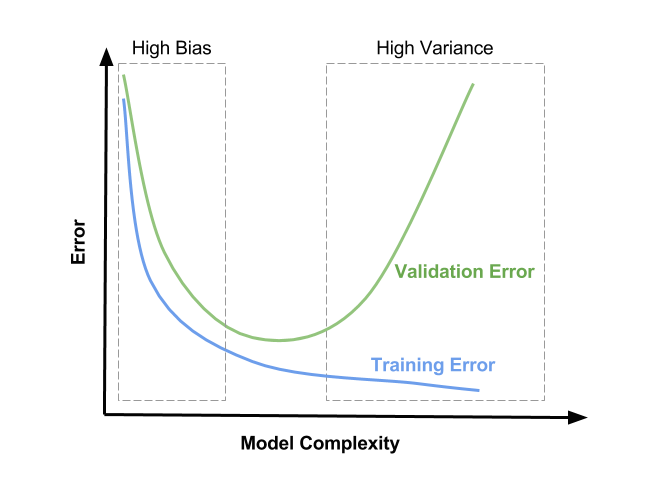

An example using pca for dimensionality reduction while maintaining an amount of variance.

Cv mat variance. Cv getcv x compute the coefficient of variation c v of the input vector x. Input vector output cv. The function ignores nans. If a is a matrix whose columns are random variables and whose rows are observations v is a row vector containing the variances corresponding to each column.

Github is home to over 50 million developers working together to host and review code manage projects and build software together. Cv vl where the covariance matrix can be represented as c vlv 1 which can be also obtained by singular value decomposition. If a is a multidimensional array then var a treats the values along the first array dimension whose size does not equal 1 as vectors. In probability theory and statistics a covariance matrix also known as auto covariance matrix dispersion matrix variance matrix or variance covariance matrix is a square matrix giving the covariance between each pair of elements of a given random vector in the matrix diagonal there are variances i e the covariance of each element with itself.

If a is a vector of observations the variance is a scalar. Output nx1 matrix with computed variance. The eigenvectors are unit vectors representing the direction of the largest variance of the data while the eigenvalues represent the magnitude of this variance in the corresponding directions. Computes the mean and variance of a given matrix along its rows.

In our example the variance was 200 therefore standard deviation is 14 14. Output nx1 matrix with computed mean. Vice versa variance is standard deviation squared. It computes in the same way as woud do reduce but with variance function.

Coefficient of variation a scalar. To calculate standard deviation from variance only take the square root. Dismiss join github today.

Cost Variance Formula In 2020 Earned Value Management Cost Accounting Analysis

Z 5 Sum Of Squares Variance And The Standard Error Of The Mean Westgard

Opencv Cv Img Hash Radialvariancehash Class Reference

What S The Theory Behind Computing Variance Of An Image Stack Overflow

Poster Designs Color Design Typography Theory Con Imagenes Tipografia Disenos De Unas Diseno Grafico

Mean Variance Coefficient Of Skewness And Excess Kurtosis For The Download Table

Combined Analysis Of Variance Mean Square For Effect Of Pruning And Download Table

Variance Analysis In Excel Making Better Budget Vs Actual Charts Pakaccountants Com Microsoft Excel Tutorial Excel Tutorials Microsoft Excel Formulas

A Sample Income Statement Modified For Budget Variance Analysis Income Statement Financial Analysis Cost Accounting

Click Here To Download This Financial Analyst Resume Template Http Www Resumetemplates101 Com Fina Business Analyst Resume Business Analyst Executive Resume

Pdf Can Analysis Of Variance Be More Significant

Coefficient Of Variance Cv Of Common Size Items Download Table

Cover Letter Template Accounting Accounting Cover Coverlettertemplate Letter Tem Cover Letter Example Job Cover Letter Examples Cover Letter For Resume